India's pension landscape has seen significant shifts in recent years, with the government introducing new schemes and reforming existing ones. This article explores three key pension schemes: the Old Pension Scheme (OPS), the National Pension System (NPS), and the newly introduced Unified Pension Scheme (UPS).

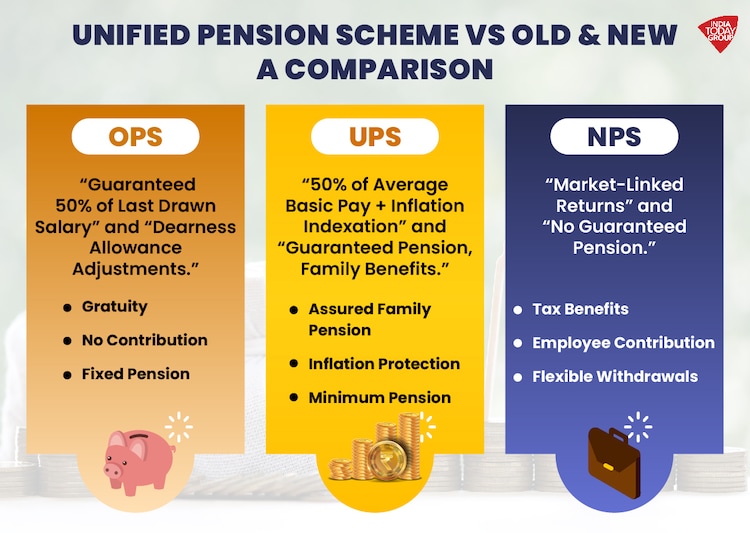

| Feature | Old Pension Scheme (OPS) | National Pension System (NPS) | Unified Pension Scheme (UPS) |

|---|---|---|---|

| Eligibility | Government employees who joined service before 2004 | All Indian citizens aged 18-70 | Central Government employees (applicable from April 1, 2025) |

| Pension Amount | 50% of last drawn salary with DA hikes | Market-linked returns (varies) | 50% of average basic pay (last 12 months) |

| Employee Contribution | None | 10% of basic salary | 10% of basic salary |

| Government Contribution | 100% | 14% of basic salary | 18.5% of basic salary |

| Inflation Protection | Yes, through DA hikes | No automatic adjustment | Yes, adjusted by AICPI-IW |

| Investment Options | Not applicable | Equity, corporate bonds, government securities | Combination of assured returns and market-linked investments |

| Risk | No investment risk | Market-linked investments carry risk | Lower risk compared to NPS due to assured component |

| Flexibility | Less flexible | More investment flexibility | Less flexible than NPS |

| Key Features | Guaranteed pension, DA hikes | Potential for higher returns, tax benefits | Guaranteed pension, inflation protection, family pension |

1. The Old Pension Scheme (OPS)

2. The National Pension System (NPS)

3. The Unified Pension Scheme (UPS)

Choosing the Right Scheme

The best pension scheme depends on individual risk tolerance, financial goals, and long-term objectives.

Disclaimer: This information is for general knowledge and does not constitute financial advice. It's crucial to consult with a qualified financial advisor to determine the most suitable pension scheme for your individual circumstances.

Key Considerations:

By carefully evaluating your needs and preferences, you can make an informed decision about the most appropriate pension scheme for your retirement planning.

Sources and related content

🕑 28 Oct, 2025 04:46 PM

🕑 28 Oct, 2025 04:46 PM

8th Pay Commission constituted. ToR Approved, Effectively Jan 2026

🕑 02 Jul, 2025 10:03 AM

🕑 02 Jul, 2025 10:03 AM

Commutation Relief In Sight? Panel Likely To Review 15-Year Deduction Rule

🕑 12 Jun, 2025 08:12 AM

🕑 12 Jun, 2025 08:12 AM

8th Pay Commission: Uncertainty Looms as Employees Await Terms of Reference

🕑 24 Apr, 2025 10:21 PM

🕑 24 Apr, 2025 10:21 PM

Staff Side constitutes panel for drafting memorandum to 8th CPC when formed

🕑 24 Apr, 2025 10:17 PM

🕑 24 Apr, 2025 10:17 PM

8th Pay Commission likely to be set up by mid May

🕑 09 Apr, 2025 10:27 AM

🕑 09 Apr, 2025 10:27 AM

Loan EMIs to get Cheaper as RBI cuts Repo Rate sgain | See the benefit

🕑 09 Jun, 2025 08:25 AM

🕑 09 Jun, 2025 08:25 AM

📢 UPS vs NPS: The Retirement Dilemma Facing 27 Lakh Government Employees

🕑 04 Apr, 2025 04:46 PM

🕑 04 Apr, 2025 04:46 PM

NPS To UPS Switch from April 1: A Detailed Look at the Option to Switch

🕑 30 Mar, 2025 11:01 AM

🕑 30 Mar, 2025 11:01 AM

8th Pay Commission implementation may get delayed till 2027 – Here’s why

🕑 27 Mar, 2025 10:25 PM

🕑 27 Mar, 2025 10:25 PM

7th CPC wanted a permanent pay panel, end DA revision twice

🕑 27 Mar, 2025 08:43 AM

🕑 27 Mar, 2025 08:43 AM

8th Pay Commission: What Kind Of Salary Hike Can Be Staff Expected?

🕑 20 Mar, 2025 08:24 AM

🕑 20 Mar, 2025 08:24 AM

Why the commuted pension is restored after 15 years, not 12 years

🕑 17 Mar, 2025 08:37 AM

🕑 17 Mar, 2025 08:37 AM

📈 Expected Dearness Allowance (DA) from January 2026 Calculator